Lego is one of those brands that feels like it's always been massive. But if you look at the data, the Lego of 2025 is a fundamentally different business to the Lego of 2005. I pulled the Brickset dataset covering every Lego set from 1970 to 2025 — to understand what's actually behind the growth.

The question was simple: is Lego's dominance driven by one thing, or has the whole model shifted?

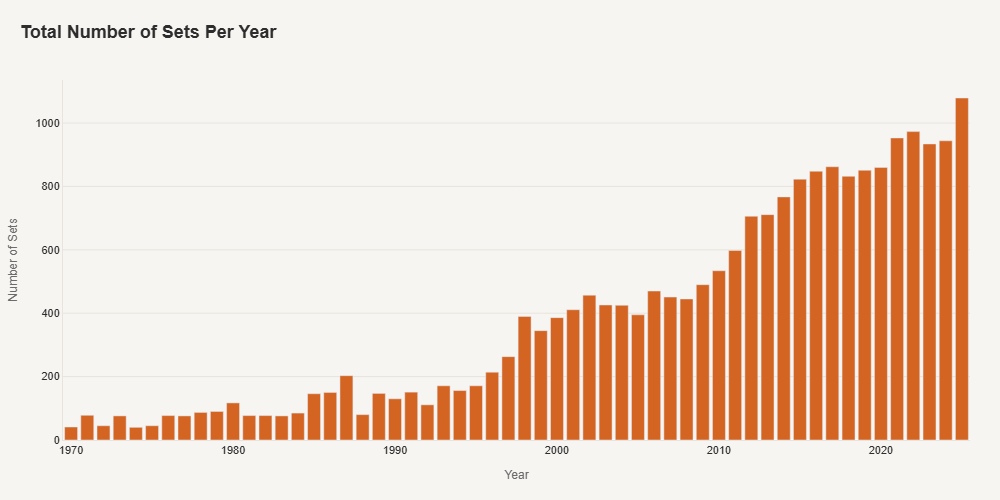

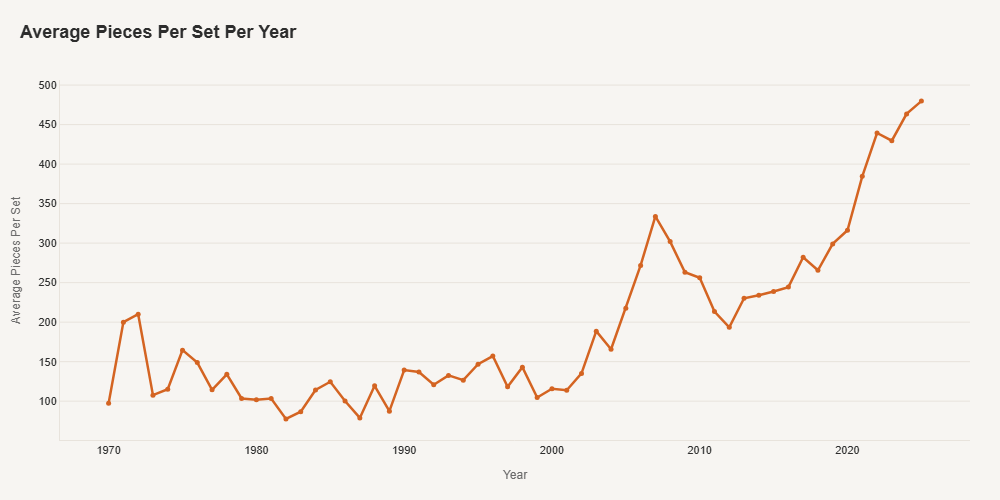

More sets, bigger sets

The most obvious trend is volume. Lego has dramatically increased the number of sets launched per year over the last two decades. But it's not just more sets — the sets themselves are getting bigger. If you bought an average Lego set in 2012 and compared it to an average set in 2025, the 2025 set would be around 280 pieces larger.

More sets, more pieces per set. That's the first layer.

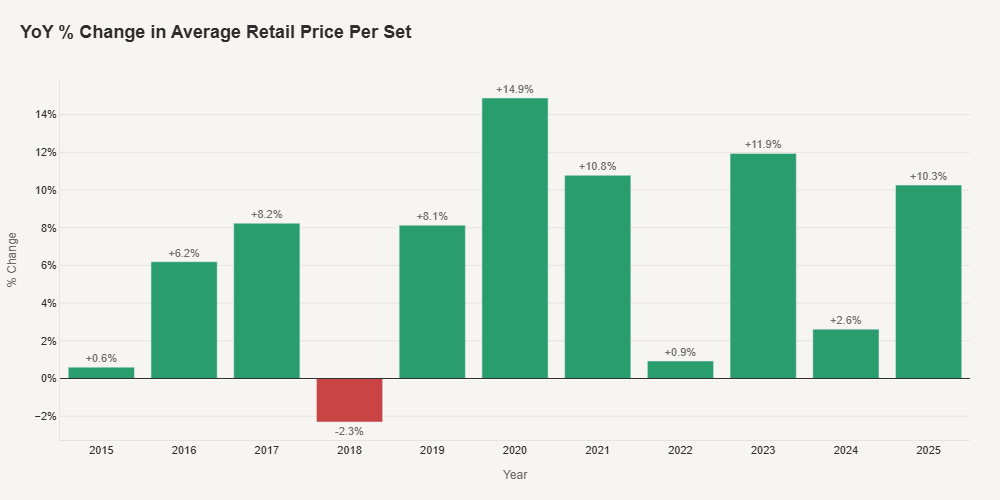

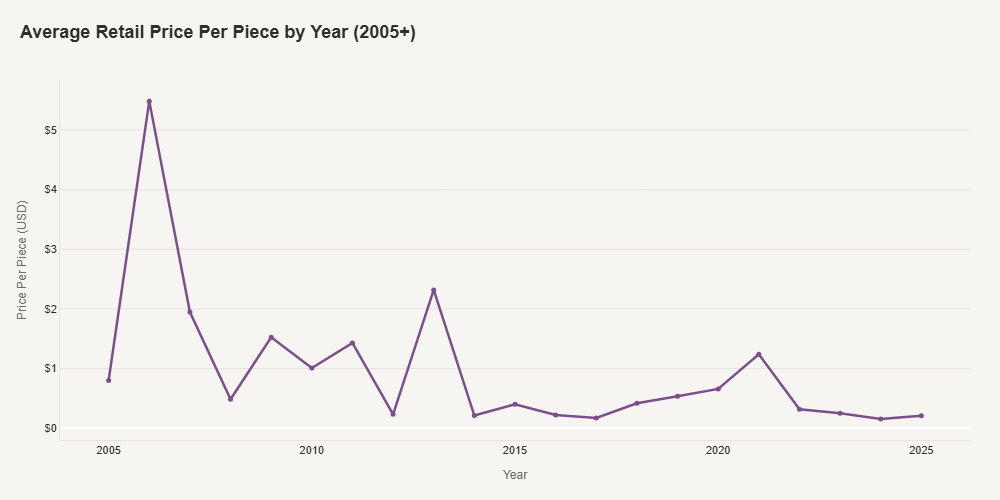

Prices are up, but value per piece is down

Per-set prices have been climbing steadily. Since 2015, the average retail price has increased by roughly +6.5% per year. That sounds like straightforward inflation — but there's a twist.

The price per piece has actually been falling. Lego is giving consumers more value on a per-piece basis even while the sticker price goes up. The sets are bigger, so the total cost is higher, but the unit economics have shifted in the consumer's favour.

This is a classic premiumisation play: raise the average transaction value by giving more product, not by charging more for the same thing.

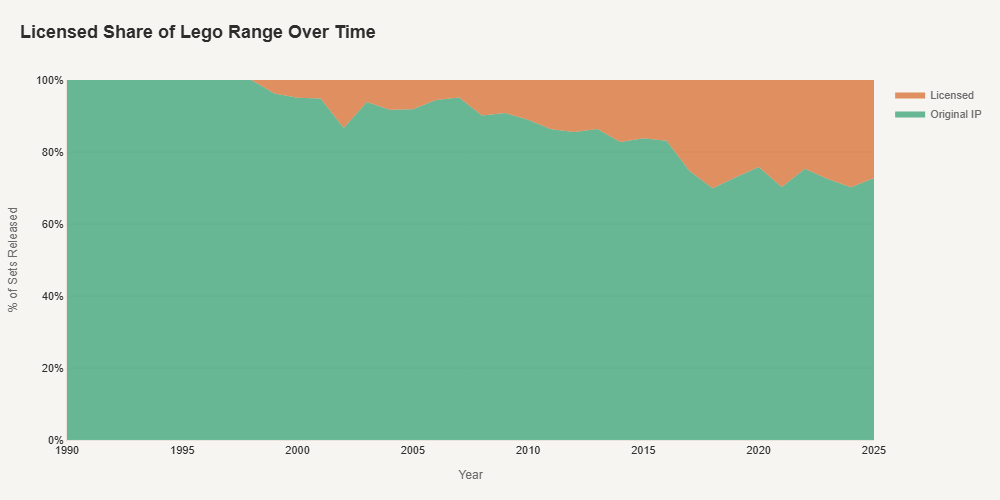

The licensed IP shift

Here's where it gets interesting. Licensed IP — Star Wars, Harry Potter, Marvel, and so on — now makes up 30% of the Lego range, up from roughly 10% in 2005. That's a massive strategic shift.

Licenses have been a major growth driver for new launches and they command higher price points. Consumers are willing to pay more for a branded set than a generic one, and Lego has leaned into this heavily.

But there's a risk embedded in this strategy. When 30% of your range depends on third-party IP, you're exposed to contract negotiations, margin pressure, and the risk that a licence doesn't renew. It's growth, but it's growth with strings attached.

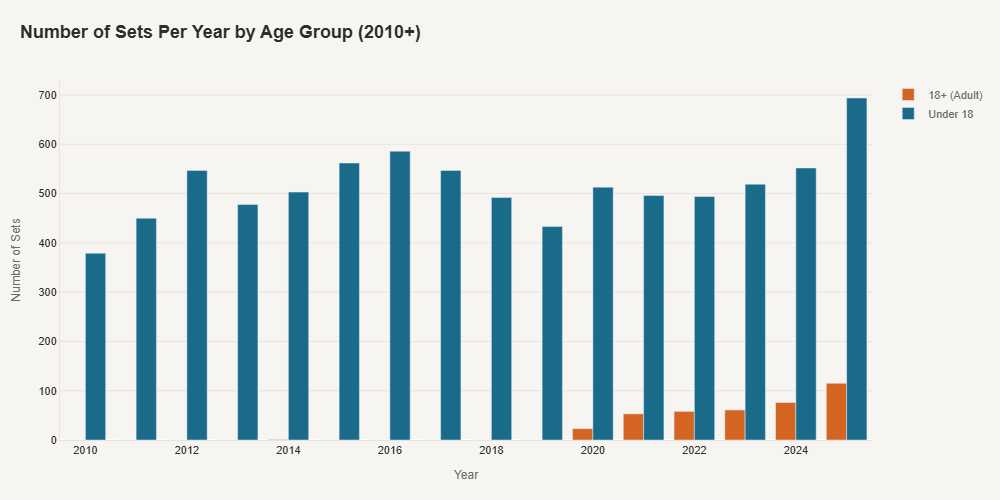

The adult market

The other major shift has been Lego's investment in sets tailored specifically for adults, particularly since 2020. Adults have a higher willingness to pay, and the average price point for adult-targeted sets is significantly higher than the core children's range.

This is where the price increases are really coming from. It's not that Lego is charging kids more for the same sets — it's that the product mix has shifted toward a higher-spending demographic.

What it means

Lego's growth story isn't a single factor. It's three things compounding:

- Volume: more sets launched per year

- Licensed IP: 30% of the range now depends on branded partnerships, driving both launches and premiumisation

- The adult market: a higher willingness to pay from a new demographic, shifting the average price upward

The core children's range hasn't disappeared, but it's no longer the growth engine. The growth engine is adults buying a $350 Star Wars set, not kids buying a $40 City set.

For anyone in category management or range planning, the Lego story is a textbook case of how premiumisation, licensing, and demographic expansion can compound growth — and the strategic risks that come with each.

The full slide deck with charts and data is available in the Projects section of my portfolio.